Content

If the closing stock appears within the trial balance, it means the adjustment for the closing stock has already been made. It will be represented as a current asset on the right side of the balance sheet. If the values of the adjusted purchases are provided, then the trial balance will show both the accounts for adjusted purchases and the closing stock. In that case, you will debit the depreciation expense and credit the accumulated depreciation for the same amount to reflect the asset’s net book value on the balance sheet. On the balance sheet, assets usually have a debit balance and are shown on the left side. Liability accounts and owners equity accounts typically have a credit balance and are shown on the right side.

- By having accumulated depreciation recorded as a credit balance, the fixed asset can be offset.

- Depending on the account type, the sides that increase and decrease may vary.

- Let us consider the example of a company called XYZ Ltd that bought a cake baking oven at the beginning of the year on January 1, 2018, and the oven is worth $15,000.

- If the exchange has commercial substance, the asset received is recorded on the balance sheet at either the market value of the asset received or the market value of the asset given up plus any cash paid.

- At the end of every accounting period, a depreciation journal entry is recorded as part of the usual periodic adjusting entries.

If the monetary exchange is more than the asset’s book value, updated for depreciation up to the disposal date, a gain on disposal results; if the proceeds are less, the disposal realizes a loss. Unlike a voluntary sale, involuntary conversion of assets can involve an asset exchange for monetary or non-monetary assets. Compare the cash proceeds received from the sale with the asset’s book value to determine if a gain or loss on disposal has been realized.

Record a Credit Sale

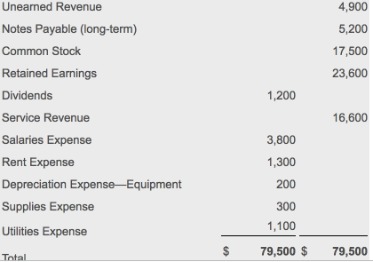

The goal of adjusting the entries is to correct errors made within previous iterations of the trial balance. Once the adjustments are made, the trial balance becomes a summary detailing all accounts within the general ledger. In the second year, you will deduct the total depreciation expense from the purchase price ($110,000 – $20,000) and follow the same formula.

- If this is not done accurately, it would be difficult to create financial statements.

- The Accumulated depreciation, on the other hand, is a contra-asset account and as such would have a natural credit balance .

- At the end of the year, Company A uses the straight-line method to calculate the depreciation for the van, arriving at an annual expense of $2,000 ($20,000 purchase price / 10 years of useful life).

- When accounting for depreciation, is depreciation expense a debit or credit?

- For example, say Poochie’s Mobile Pet Grooming purchases a new mobile grooming van.

The allowance for doubtful accounts includes a balance of the estimated amount of Accounts receivable that is uncollectible in the future . The allowance for doubtful depreciation expense credit or debit accounts is adjusted as new information is available and also at year-end. When you pay for the insurance policy, you credit cash because cash is reduced.

How to Book a Fixed Asset Depreciation Journal Entry

Now, consider that Waggy Tails decides to use the equipment at the end of 10 years. Even then, the accumulated depreciation cannot exceed the asset’s original cost, despite remaining in use after its estimated useful life. Accumulated depreciation is an accounting term used to assess the financial health of your business. This post will help you understand what accumulated depreciation means and how you can calculate it to simplify your bookkeeping. Introduction Accountants use debits and credits to record each business transaction and generate financia…

Is depreciation expense an expense or asset?

Depreciation is used on an income statement for almost every business. It is listed as an expense, and so should be used whenever an item is calculated for year-end tax purposes or to determine the validity of the item for liquidation purposes.

The cost of an asset is the purchase price of the asset and the salvage value is the estimated book value of the asset after depreciation is complete. This salvage value is based on what a company expects to receive in exchange for the asset at the end of its useful life. Let’s say as an example that Exxon Mobil Corporation has a piece of oil drilling equipment that was purchased for $1 million. Over the past three years, depreciation expense was recorded at a value of $200,000 each year.

What is double-entry bookkeeping?

Depreciation expenses a portion of the cost of the asset in the year it was purchased and each year for the rest of the asset’s useful life. Accumulated depreciation allows investors and analysts to see how much of a fixed asset’s cost has been depreciated. In some scenarios, subsequent journal entries may change due to adjustments to the fixed asset’s useful life or value to the company as a result of improvements or impairments of the asset. For example, during year 5 the company may realize the asset will only be useful for 8 years instead of the originally estimated 10 years.

It may also help them in estimating the asset’s remaining useful life. Outside of the accounting world, depreciation means the decline in value of an item after purchase. In accounting, depreciation is the process of allocating the cost of an item over its anticipated useful life. This helps to ensure that company revenues are matched with the costs of assets used by a company to generate that revenue.

How do you debit depreciation expense?

How Do I Record Depreciation? Depreciation is recorded as a debit to a depreciation expense account and a credit to a contra asset account called accumulated depreciation. Contra accounts are used to track reductions in the valuation of an account without changing the balance in the original account.